VAT stands for “Value-Added Tax.” It’s a consumption tax that applies to goods and services at each stage of the production and distribution chain. Unlike sales tax, which is typically charged only at the final point of sale to the consumer, VAT is collected incrementally at each step where value is added. In practice, businesses charge VAT to their customers and then remit it to the tax authorities, but they can also reclaim the VAT they’ve paid on their own purchases. This system helps prevent double taxation and ensures a consistent application of tax throughout the supply chain.

For non-Japanese enterprises dealing with Japan, understanding VAT is crucial because it affects pricing, compliance, and overall business strategy.

Category: Tax

Tax Audits in Japan

Tax Audit Frequency and Objectives

In Japan, tax audits are a routine part of the self-assessment system for both corporate tax and consumption tax. Approximately 100,000 corporate tax audits are conducted each year. Typically, profitable companies can expect an audit about once every five years. The primary purpose of these audits is to strengthen the self-assessment process and ensure fair taxation. The National Tax Agency (NTA) is responsible for reviewing tax returns, comparing them with the taxpayer’s financial records, and correcting any discrepancies.

Audit Process

The NTA focuses on auditing companies suspected of tax evasion, dedicating significant time to thorough investigations. The audit process generally follows these steps:

- Advance Notice of Tax Audit:

In most cases, taxpayers are notified of an upcoming audit via phone, allowing them time to prepare. However, if the NTA needs to verify certain business activities directly, advance notice may not be given. - Conducting the Audit:

Upon arrival at the taxpayer’s office or residence, tax auditors will present official identification. A successful audit relies on the taxpayer’s full cooperation, including providing transaction records and answering inquiries. While audits are typically conducted in the taxpayer’s presence, a Certified Public Tax Accountant (CPTA) can represent them if preferred. - Post-Audit Actions:

If discrepancies are found, the Tax Office will explain the errors and outline the additional tax liabilities, recommending that the taxpayer files an amended return. Failure to comply may result in the District Director issuing mandatory corrections. If no issues are identified, the Tax Office will confirm the accuracy of the return or provide advice for future submissions and record-keeping.

Statute of Limitations

The statute of limitations for corporate and consumption taxes in Japan is generally five years from the filing due date of the original return. For loss-making years, the period extends up to nine years for fiscal years ending on or before March 31, 2018, and ten years for those starting on or after April 1, 2018.

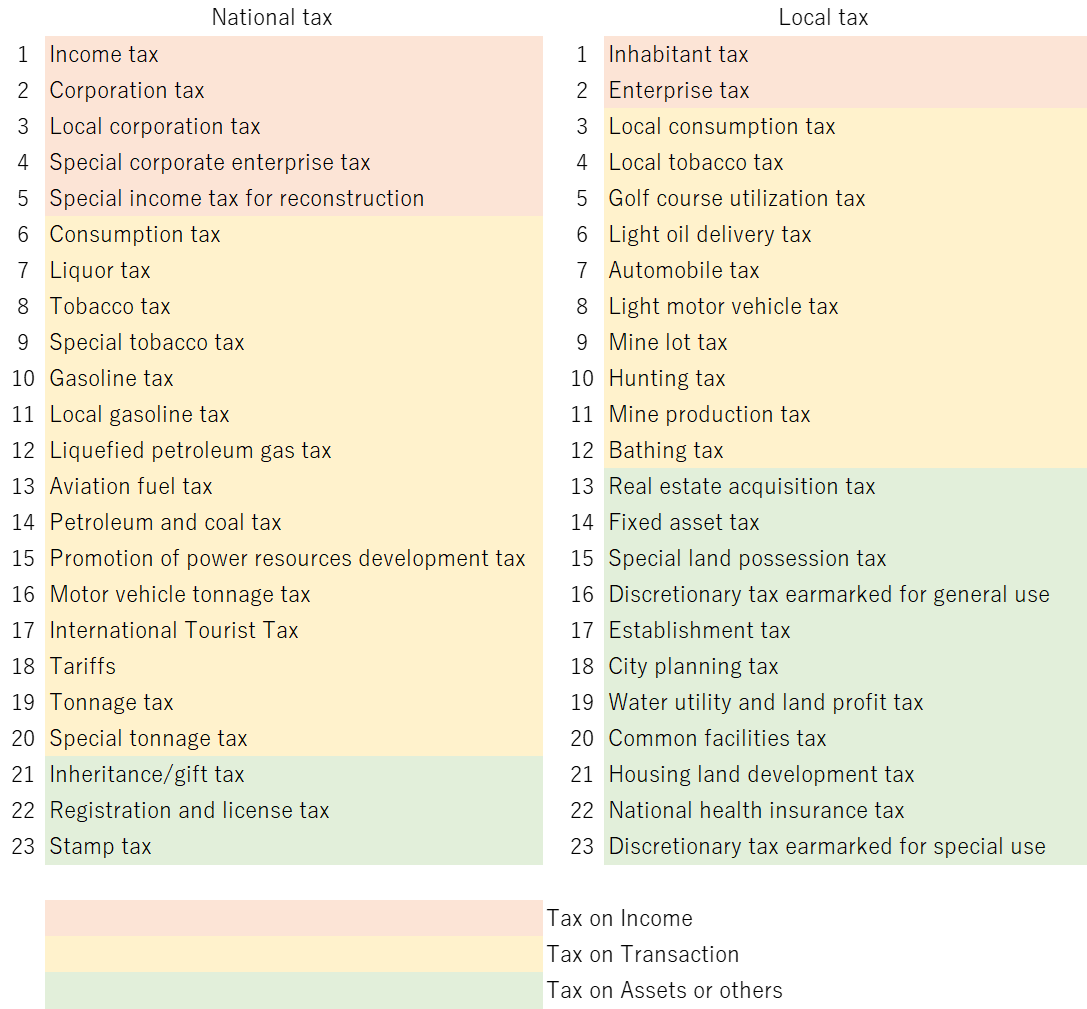

Japanese Tax Items

Japan’s tax system, while extensive with over 40 different tax items, primarily revolves around a few key areas for most taxpayers: the income taxes and the consumption tax. The system is evenly divided between national tax and local tax in terms of both the number of tax items and the overall revenue generated. Although there are various special-purpose taxes on specific goods such as liquor, tobacco, and automobiles, these tend to have less impact on the majority of individual taxpayers.

Crucially, Japan’s tax laws apply universally to all individuals, regardless of nationality. However, the tax implications for each taxpayer can vary significantly depending on the specific regulations governing each type of tax. Understanding these nuances is essential for effective tax planning and compliance, particularly for those subject to multiple tax jurisdictions or with complex financial arrangements.

In summary, while Japan’s tax structure may appear intricate at first glance, focusing on the core components, such as income and consumption taxes, simplifies the landscape for most taxpayers. A thorough understanding of the detailed regulations and how they apply to individual circumstances is critical for navigating the system effectively and ensuring compliance.

Japanese Tax Items

Deduction of social welfare contribution born by individuals for income tax purposes

The Japanese Income Tax Act defines deductible social welfare contributions, referred to as “social insurance premiums,” as follows:

- premiums for health insurance paid by the resident as an insured under the provisions of the Health Insurance Act (Act No. 70 of 1922);

- premiums for national health insurance under the National Health Insurance Act (Act No. 192 of 1958) or national health insurance tax under the provisions of the Local Tax Act;

- premiums under the provisions of the Act on Assurance of Medical Care for Elderly People (Act No. 80 of 1982);

- premiums for long-term care insurance under the provisions of the Long-term Care Insurance Act (Act No. 123 of 1997);

- labor insurance premiums paid by the resident as an insured of employment insurance under the provisions of the Act on the Collection, etc. of Insurance Premiums of Labor Insurance (Act No. 84 of 1969);

- premiums for national pension to be paid by the resident as an insured under the provisions of the National Pension Act and premiums to be paid by the resident as a member of the National Pension Fund;

- premiums for farmers pension paid by the resident as an insured under the provisions of the Act on the Farmers Pension Fund, Independent Administrative Agency;

- premiums for Employees’ pension insurance paid by the resident as an insured under the provisions of the Employees’ Pension Insurance Act;

- premiums for Mariners” insurance paid by the resident as an insured under the provisions of the Mariners’ Insurance Act;

- premiums under the provisions of the National Public Officers Mutual Aid Association Act;

- premiums (including special premiums) under the provisions of the Local Public Officers, etc. Mutual Aid Association Act;

- premiums paid by the resident as a member under the provisions of the Private School Personnel Mutual Aid Association Act; and

- payment under the provisions of Article 59 (Pension payment) of the Public Officers Pension Act (including the cases where applied mutatis mutandis pursuant to other laws).

Essentially, the above provisions clarify that only contributions to Japan’s public social welfare funds are considered deductible expenses for income tax purposes.

However, there are exceptions under tax treaties. For example, Article 18 of the Japan-France tax treaty, as modified by Article 12 of its Protocol, specifies that social insurance premiums paid to the social security system of one contracting country by individuals from the other contracting country who are working in the host country, as stipulated by the Japan-France Social Security Agreement, are mutually recognized as deductible in the country of employment.

Therefore, in very exceptional cases outlined in tax treaties and social security agreements, contributions to foreign social welfare systems may also qualify as deductible.

Taxation on Expats leaving Japan

The Final Tax Declaration as Residents

Residents:

Those who have a domicile in Japan and have resided continuously in Japan for one year or more.

Non-residents:

All individuals other than residents.

When the individual has an occupation overseas that typically requires them to reside continuously for more than one year, they are presumed to be non-residents immediately after the departure from Japan.

| Practical application of presumption of domicile (basic circular) In order to make it more practical and uniformed judgments regarding the specific application of the provision for presuming the presence or absence of a domicile, unless the period of service outside of Japan for employees working outside of Japan is limited to less than one year in advance in contracts, it is presumed that the person does not have a domicile in Japan. |

Tax Declaration at the Time of Departure

Article 127. Where a resident is to make a departure from Japan during the year, and a return under the provisions of Article 120(1) (Income tax return) needs to be filed with regard to the amount of gross income, the amount of retirement income, and the amount of timber income of the resident for the period from January 1 of the year until the time of his/her departure, the resident must file a return stating the matters listed in the items of paragraph (1) of the said Article based on the circumstances as of the relevant time with the district director of the tax office by the time of the departure, ….

Definitions under Article 2, Paragraph 1 of the Income Tax Law

(xlii) departure: with regard to a resident, to cease to have a domicile or a residence in Japan without making a notification of tax administrator under the provisions of Article 117(2) (Tax administrators) of the Act on General Rules for National Taxes, and with regard to a nonresident, to cease to have a residence in Japan without making a notification of tax administrator under the said paragraph (with regard to a nonresident who does not have a residence but has a permanent establishment in Japan, this term means that such nonresident ceases to have a permanent establishment, and with regard to a nonresident who does not have a residence nor a permanent establishment in Japan, this term means that such nonresident discontinues the business prescribed in Article 161(1)(vi) (Domestic source income) that the nonresident conducts in Japan);

Cases Not Requiring Final Income Declaration According to Article 121 of the Income Tax Law

Article 121. Notwithstanding the provisions of paragraph (1) of the preceding Article, where a resident who has employment income for the year and whose salary, etc. prescribed in Article 28(1) (Employment income) (hereinafter referred to as a “salary, etc.” in this paragraph) to be received within the year is not more than 20,000,000 yen falls under any of the following items, the resident is not required to file a return under the provisions of paragraph (1) of the preceding Article with regard to the income tax related to the amount of taxable gross income and the amount of taxable timber income for the year; provided, however, that this shall not apply in cases specified by Cabinet Order, such as where the resident receives payment of consideration for providing his/her assets, such as real property for the business of the payer of the salary, etc. related to the employment income :

i. where the resident has received payment of a salary, etc. from one payer of salary, etc. and income tax has been withheld or is to be withheld pursuant to the provi-sions of Article 183 (Withholding liability for employment income) or Article 190 (Year-end adjustment) with regard to the whole of the said salary, etc., and if the sum of the amount of interest income, the amount of dividend income, the amount of real property income, the amount of business income, the amount of timber income, the amount of capital gains income, the amount of occasional income, and the amount of miscellaneous income (hereinafter referred to as the “amount of income other than employment income and retirement income” in this paragraph) is not more than 200,000 yen

Tax Agent/Administrator

Under Article 117 of the National Tax Agency Law (Tax Agent/Administrator), individuals who do not have a domicile or residence (excluding offices and business places) in the enforcement area of this law, or corporations without a head office or main office in the enforcement area, must appoint a tax agent to handle submissions of tax returns and other tax-related matters when necessary.

Appointing a tax agent subjects the individual to the regular tax declaration deadlines, not the deadlines applicable at the time of departure.

Tax Agent for Municipal Taxes under Article 300 of the Local Tax Law

Taxpayers of municipal taxes must appoint a tax agent to handle all tax-related matters if they do not have a domicile, residence, office, business place, or dormitory within the municipality. They must report this agent to the mayor or apply for approval to appoint an agent from outside the designated area who is convenient for handling such matters. Changing the tax agent is subject to similar regulations. However, if the taxpayer can prove to the mayor that appointing a tax agent is not necessary for the secure collection of municipal taxes, then appointing one is not required.

Year-End Adjustment at the Time of Departure

Article 190. With regard to a resident who has submitted an employment income earner’s declaration for dependency deduction, etc. and for whom the amount of salary, etc. that is determined to be paid during the year as prescribed in item (i) is not more than 20,000,000 yen, where the payer of salary, etc. via whom the resident has submitted the said declaration makes the last payment of salary, etc. for the year (excluding the case where the resident is expected to submit the said declaration to a payer other than the said payer thereafter by December 31 of the year), if the total amount of income tax set forth in the said item exceeds or falls below the amount of tax set forth in item (ii) as calculated based on the circumstances at the time of the last payment of salary, etc. for the year, the amount of excess must be appropriated to income tax to be withheld upon the last payment of salary, etc. for the year, and the amount of shortfall must be withheld upon the last payment of salary, etc. for the year and paid to the State by the tenth day of the month following the month in which the day of withholding falls:

Notification Related to Affiliation

Foreign nationals working with a work permit must submit a “Notification Related to Affiliation” to the Immigration Bureau upon resigning from their company. The resigned foreign national must fill out the prescribed form with their name, date of birth, gender, nationality, address, residence card number, the name and location of the resigned company, and the resignation date, and submit it to the Immigration Bureau.

外国人の帰任時の課税関係

居住者としての最後の申告

・出国時確定申告

所得税法127条(年の中途で出国をする場合の確定申告)

居住者は、年の中途において出国をする場合において、その年一月一日からその出国の時までの間における総所得金額、退職所得金額及び山林所得金額について、第百二十条第一項(確定所得申告)の規定による申告書を提出しなければならない場合に該当するときは、中略、その出国の時までに、税務署長に対し、その時の現況により同条第一項各号に掲げる事項を記載した申告書を提出しなければならない。

所得税法2条1項(定義)

四十二 出国 居住者については、国税通則法第百十七条第二項(納税管理人)の規定による納税管理人の届出をしないで国内に住所及び居所を有しないこととなることをいい、非居住者については、同項の規定による納税管理人の届出をしないで国内に居所を有しないこととなること(国内に居所を有しない非居住者で恒久的施設を有するものについては、恒久的施設を有しないこととなることとし、国内に居所を有しない非居住者で恒久的施設を有しないものについては、国内において行う第百六十一条第一項第六号(国内源泉所得)に規定する事業を廃止することとする。)をいう。

所得税法121条 (確定所得申告を要しない場合)

その年において給与所得を有する居住者で、その年中に支払を受けるべき第28条第1項(給与所得)に規定する給与等(以下この項において「給与等」という。)の金額が2000万円以下であるものは、次の各号のいずれかに該当する場合には、前条第1項の規定にかかわらず、その年分の課税総所得金額及び課税山林所得金額に係る所得税については、同項の規定による申告書を提出することを要しない。ただし、不動産その他の資産をその給与所得に係る給与等の支払者の事業の用に供することによりその対価の支払を受ける場合その他の政令で定める場合は、この限りでない。

一 一の給与等の支払者から給与等の支払を受け、かつ、当該給与等の全部について第183条(給与所得に係る源泉徴収義務)又は第190条(年末調整)の規定による所得税の徴収をされた又はされるべき場合において、その年分の利子所得の金額、配当所得の金額、不動産所得の金額、事業所得の金額、山林所得の金額、譲渡所得の金額、一時所得の金額及び雑所得の金額の合計額(以下この項において「給与所得及び退職所得以外の所得金額」という。)が20万円以下であるとき。

・納税管理人

国税通則法117条(納税管理人)

個人である納税者がこの法律の施行地に住所及び居所(事務所及び事業所を除く。)を有せず、若しくは有しないこととなる場合又はこの法律の施行地に本店若しくは主たる事務所を有しない法人である納税者がこの法律の施行地にその事務所及び事業所を有せず、若しくは有しないこととなる場合において、納税申告書の提出その他国税に関する事項を処理する必要があるときは、その者は、当該事項を処理させるため、この法律の施行地に住所又は居所を有する者で当該事項の処理につき便宜を有するもののうちから納税管理人を定めなければならない。

納税管理人を定めた場合には、出国時ではなく通常の申告期限に従った確定申告が適用されることとなる。

地方税法第300条(市町村民税の納税管理人)

市町村民税の納税義務者は、納税義務を負う市町村内に住所、居所、事務所、事業所又は寮等を有しない場合においては、納税に関する一切の事項を処理させるため、当該市町村の条例で定める地域内に住所、居所、事務所若しくは事業所を有する者のうちから納税管理人を定めてこれを市町村長に申告し、又は当該地域外に住所、居所、事務所若しくは事業所を有する者のうち当該事項の処理につき便宜を有するものを納税管理人として定めることについて市町村長に申請してその承認を受けなければならない。納税管理人を変更し、又は変更しようとする場合においても、また、同様とする。

2 前項の規定にかかわらず、当該納税義務者は、当該納税義務者に係る市町村民税の徴収の確保に支障がないことについて市町村長に申請してその認定を受けたときは、納税管理人を定めることを要しない。

・出国時年末調整

所得税法第190条(年末調整)

給与所得者の扶養控除等申告書を提出した居住者で、第一号に規定するその年中に支払うべきことが確定した給与等の金額が二千万円以下であるものに対し、その提出の際に経由した給与等の支払者がその年最後に給与等の支払をする場合(その居住者がその後その年十二月三十一日までの間に当該支払者以外の者に当該申告書を提出すると見込まれる場合を除く。)において、同号に掲げる所得税の額の合計額がその年最後に給与等の支払をする時の現況により計算した第二号に掲げる税額に比し過不足があるときは、その超過額は、その年最後に給与等の支払をする際徴収すべき所得税に充当し、その不足額は、その年最後に給与等の支払をする際徴収してその徴収の日の属する月の翌月十日までに国に納付しなければならない。

非居住者となる月の源泉徴収 通達185−5

控除額の計算 タックスアンサー No.1920

・所属機関等の関する届出

就労在留許可証を持って働く外国人が雇用先の企業を退職したときには、「所属機関等の関する届出」を入管に提出することが必要になります。退職した外国人本人が、自身の氏名、生年月日、性別、国籍、住所、在留カード番号などに加えて、退職した会社の名称と所在地、退職日を所定の様式に記入して、入管に提出します。

「非居住者に支払われる給与、報酬、年金及び賞金の支払調書」への記載金額

「非居住者に支払われる給与、報酬、年金及び賞金の支払調書」については、記載要領において「支払調書は、非居住者及び外国法人に支払う法第161 条第1項第12号に掲げる給与、報酬又は年金及び同項第13 号に掲げる賞金について使用する」ものとして、国内源泉所得に係るものだけが記載されることが想定されているものといえる。

この場合には居住者、非居住者を区分しない源泉徴収票上の支払いがある場合には、その内容が重複するものともいえる。

ここでは、例えば、非居住者に対して、国内において行う人的役務の提供の対価として給与等の支払をした場合には、「給与所得の源泉徴収票」ではなく、「非居住者に支払われる給与、報酬、年金及び賞金の支払調書」を提出する必要があるとされている。

源泉徴収票は3つの所得種類のみに限られており法定調書の範囲(第161条第1項第4号若しくは第6号から第16号までに掲げる国内源泉所得又は第209条第2号)が源泉徴収範囲よりも大きいことからそちらが優先されるという形での整理であるものと考えられる。

年の途中で居住者 確定申告

給与所得者が1年以上の予定で海外の支店などに転勤すると、一般的には、日本国内に住所を有しない者と推定され、所得税法上の非居住者となります。

非居住者の場合、国内源泉所得(例えば、国内不動産の賃貸料収入など)のみが課税対象とされ、日本の法人の役員の場合を除き海外勤務に基づき支給される給与は課税されません。

しかし、非居住者に該当していた海外勤務者が、日本に帰国した後は居住者となりますので、居住者となる帰国後は国内源泉所得に限らずすべての所得が課税の対象となります。

なお、帰国後の勤務に対する給与については年末調整の対象になります。

したがって、帰国した年分の確定申告は帰国前の国内源泉所得(源泉分離課税となるものを除きます。)と帰国後のすべての所得を合計して計算することになります。

(年の中途で非居住者が居住者となつた場合の税額の計算)

第百二条 その年十二月三十一日(その年の中途において死亡した場合には、その死亡の日)において居住者である者でその年において非居住者であつた期間を有するもの又はその年の中途において出国をする居住者でその年一月一日からその出国の日までの間に非居住者であつた期間を有するものに対して課する所得税の額は、前二章(課税標準及び税額の計算)の規定により計算した所得税の額によらず、居住者であつた期間内に生じた第七条第一項第一号(居住者の課税所得の範囲)に掲げる所得(非永住者であつた期間がある場合には、当該期間については、同項第二号に掲げる所得)並びに非居住者であつた期間内に生じた第百六十四条第一項各号(非居住者に対する課税の方法)に掲げる非居住者の区分に応ずる同項各号及び同条第二項各号に掲げる国内源泉所得に係る所得を基礎として政令で定めるところにより計算した金額による。

注意事項

確定申告に際して適用する各種所得控除について、以下の点にご注意ください。

1 医療費控除、社会保険料控除、小規模企業共済等掛金控除、生命保険料控除、地震保険料控除の各控除の額は、居住者期間(帰国後)に支払ったこれらの金額を基として計算します。

2 配偶者(特別)控除、扶養控除、障害者控除、寡婦控除、ひとり親控除および勤労学生控除の各控除の額は、その年の12月31日の現況により判定したところで計算します。

根拠法令等

所法2、5、7、8、102、120、121、161、165、190、所令14、15、258

非居住者に対して支払われる退職金

非居住者に支払われる給与、報酬、年金及び賞金の支払調書

非居住者に対して、国内において行う人的役務の提供の対価として退職手当等の支払をした場合には、「退職所得の源泉徴収票」ではなく、「非居住者に支払われる給与、報酬、年金及び賞金の支払調書」を提出する必要があります。ただし、支払金額が年間50万円以下の場合には、提出する必要はありません。

支払の確定した年の翌年の1月31日までに、支払調書合計表とともに提出します。

なお、租税条約等により日本と自動的情報交換を行うことができる各国等に住所がある方の支払調書については、2枚提出する必要があります。

(分離課税に係る所得税の課税標準)

第百六十九条 第百六十四条第二項各号(非居住者に対する課税の方法)に掲げる非居住者の当該各号に定める国内源泉所得については、他の所得と区分して所得税を課するものとし、その所得税の課税標準は、その支払を受けるべき当該国内源泉所得の金額(次の各号に掲げる国内源泉所得については、当該各号に定める金額)とする。

中略

(分離課税に係る所得税の税率)

第百七十条 前条に規定する所得税の額は、同条に規定する国内源泉所得の金額に百分の二十(当該国内源泉所得の金額のうち第百六十一条第一項第八号及び第十五号(国内源泉所得)に掲げる国内源泉所得に係るものについては、百分の十五)の税率を乗じて計算した金額とする。

非居住者時代に稼得した退職金を帰国後に得た場合の日本での課税

Scenario A

帰国後支給 一般の「退職所得の源泉徴収票」(全世界所得)の個人と税務署(役員の場合のみ)への提出

Scenario B

帰国前支給 「退職所得の源泉徴収票」(国内源泉所得)の個人と「非居住者に支払われる給与、報酬、年金及び賞金の支払調書」の税務署(役員の場合のみ)への提出

(退職所得についての選択課税)

第百七十一条 第百六十九条(課税標準)に規定する非居住者が第百六十一条第一項第十二号ハ(国内源泉所得)の規定に該当する退職手当等(第三十条第一項(退職所得)に規定する退職手当等をいう。以下この節において同じ。)の支払を受ける場合には、その者は、前条の規定にかかわらず、当該退職手当等について、その支払の基因となつた退職(その年中に支払を受ける当該退職手当等が二以上ある場合には、それぞれの退職手当等の支払の基因となつた退職)を事由としてその年中に支払を受ける退職手当等の総額を居住者として受けたものとみなして、これに第三十条及び第八十九条(税率)の規定を適用するものとした場合の税額に相当する金額により所得税を課されることを選択することができる。

選択課税を選択した場合には、居住者としての申告として退職所得に係る全世界所得について申告を行うなければならないものとなる。

したがって、この場合には厳密には所得発生時にはまだ非居住者であったものの、日本の税制としては、居住者としての全世界所得課税により、所得税法上(または租税条約上)本来的には課税権のない所得(非居住者の国外源泉所得)について課税を行い、恣意的な2重課税を形成するものとなっているといえる。

そもそもシナリオAにおいては、所得発生時にはまだ非居住者であったものの支給時に居住者となった者について、日本の税制としては、居住者としての源泉徴収課税(または選択課税)により、本来的には所得税法上(または租税条約上)課税権のない所得(非居住者の国外源泉所得)について課税を行い、恣意的な2重課税を形成しているものともいえる。

国外居住親族に係る扶養控除等

国外居住親族に係る扶養控除等

居住者が、国外居住親族について扶養控除、配偶者控除、障害者控除又は配偶者特別控除 (以下「扶養控除等」といいます。)の適用を受けるためには、給与等又は公的年金等の支払者に一定の確認書類(親族関係書類・送金関係書類)の提出又は提示 をする必要があります。

国外居住親族

非居住者(国内に住所を有せず、かつ、現在まで引き続いて1年以上居所を有しない個人)である親族(民法の規定による親族?六親等内の血族、?配偶者、?三親等内の姻族)に該当する者をいいます。

≪配偶者控除、配偶者特別控除又は障害者控除に係る確認書類≫

扶養控除等申告書等の 提出時に必要な確認書類

年末調整時に 必要な確認書類

配偶者控除、 配偶者特別控除

「親族関係書類」 ※ 源泉控除対象配偶者に該当 する場合のみ控除可

「親族関係書類」及び 「送金関係書類」(注)

障害者控除

「親族関係書類」

「送金関係書類」

(注) 年末調整の際、配偶者控除等申告書の提出時に、これらの確認書類の提出又は提示をする必要があり ます。 なお、扶養控除等申告書を提出する際に、非居住者である配偶者について、「親族関係書類」を給与等 の支払者に提出又は提示した場合には、配偶者控除等申告書の提出の際に、「親族関係書類」を給与等の 支払者に提出又は提示する必要はありません。

≪扶養控除に係る確認書類≫

扶養控除等申告書 等(注)の提出時に 必要な確認書類

年末調整時 に 必 要 な 確 認 書 類

16 歳以上 30 歳未満 又 は 7 0 歳 以 上

「親族関係書類」

「送金関係書類」

30 歳 以 上 70 歳 未 満

? 留学により国内に住所及び 居所を有しなくなった者

「親族関係書類」 及び「留学ビザ等 書類」

「送金関係書類」

? 障害者

「親族関係書類」

「送金関係書類」

? その居住者からその年にお いて生活費又は教育費に充て るための支払を38万円以上受 けている者

「親族関係書類」

「38 万円送金 書類」

(上記?〜?以外の者)

(扶養控除の対象外)

(注) 扶養控除等申告書等とは、「給与所得者の扶養控除等(異動)申告書」又は「従たる給与についての 扶養控除等(異動)申告書」をいいます。以下同じです。

親族関係書類

?又は?のいずれかの書類で、国外居住親族が居住者の親族 であることを証するものをいいます(その書類が外国語で作成されている場合には、その翻 訳文を含みます。)。

? 戸籍の附票の写しその他の国又は地方公共団体が発行した書類及び国外居住親族の旅 券(パスポート)の写し

? 外国政府又は外国の地方公共団体が発行した書類(国外居住親族の氏名、生年月日及び 住所又は居所の記載があるものに限ります。)

送金関係書類

次の書類で、居住者がその年において国外居住親族の生活費又は 教育費に充てるための支払を必要の都度、各人に行ったことを明らかにするものをいいます (その書類が外国語で作成されている場合には、その翻訳文を含みます。)。

? 金融機関(注1)の書類又はその写しで、その金融機関が行う為替取引により居住者から国 外居住親族に支払をしたことを明らかにする書類

? いわゆるクレジットカード発行会社の書類又はその写しで、国外居住親族がそのクレジ ットカード発行会社が交付したカードを提示等してその国外居住親族が商品等を購入し たこと等により、その商品等の購入等の代金に相当する額の金銭をその居住者から受領し、 又は受領することとなることを明らかにする書類

? 電子決済手段等取引業者(注2)(電子決済手段を発行する一定の銀行等又は資金移動業者 を含みます。)の書類又はその写しで、その電子決済手段等取引業者が行う電子決済手段 の移転により居住者から国外居住親族に支払をしたことを明らかにする書類 (注1) 金融機関には、資金決済に関する法律第2条第3項に規定する資金移動業者も含まれます。

(注2) 「電子決済手段等取引業者」とは、電子決済手段の売買又は他の電子決済手段との交換やこれら の行為の媒介、取次ぎ又は代理などの電子決済手段等取引業を行う者として、内閣総理大臣の登録 を受けた者をいいます。また、「電子決済手段」とは、いわゆるステーブルコインのうち法定通貨の 価値と連動した価格で発行され、発行価格と同額で償還を約するもの及びこれに準ずる性質を有す るものとして、資金決済に関する法律第2条第5項に掲げる電子情報処理組織を用いて移転するこ とができる財産的価値などをいいます。